La semana pasada tuve el honor de poder participar como panelista y como supervisor de los talleres de capacitación en la reunión sobre financiamiento de la Agenda 2030 en el ámbito subnacional. Mi presentación ejemplificó las formas en que las alianzas público-privadas bien utilizadas pueden financiar desde proyectos comunitarios hasta grandes proyectos de infraestructura municipal o estatal.

El 2 y 3 de diciembre del 2019 participé en la reunión “Financiamiento para el Desarrollo Sostenible en el Ámbito Subnacional” y en su “Cuarta Capacitación sobre la Implementación de la Agenda 2030 en el Ámbito Subnacional” en Villahermosa, Tabasco. Quiero compartir algunos puntos importantes presentados, y aprovechar el espacio para detallar algunos aspectos que por cuestión de tiempo no pude profundizar.

Para utilizar correctamente las alianzas público-privadas, éstas deben construirse sobre la base de principios y valores éticos para implementarlas de forma armónica con los 17 Objetivos de Desarrollo Sostenible (ODS) y con la Agenda de Acción de Addis Abeba de la ONU. En mi tesis doctoral identifiqué 13 principios aplicables a las alianzas público privadas, los cuales no reproduzco aquí pero se resumen en que reflejan una teoría de justicia pura, y sobretodo enfatizan la necesidad de aumentar la transparencia así como la rendición de cuentas de las alianzas[1]. Bien vale mencionar que mi equipo de investigación en Ethos utilizó estos principios para proponer un nuevo esquema de asociación público privada en México en la reciente publicación “Transparencia y Rendición de Cuentas de las APP: Recomendaciones de Política Pública”[2].

Aquí me siento obligado a abrir un paréntesis, para dejar claro que desde mi perspectiva el concepto de ‘asociaciones público privadas’ está subsumido en el concepto de ‘alianzas público privadas’. No es una discusión bizantina tipo si decimos ‘patata’ o decimos ‘potato’. Cuando la ONU lanzó a las alianzas público privadas como uno de los instrumentos para el desarrollo sostenible, no estaba pensando únicamente en el financiamiento de proyectos de infraestructura (project finance), sino también en intervenciones sociales, proyectos, programas y políticas públicas que requieren una plataforma multiactor para poder ser articuladas exitosamente.

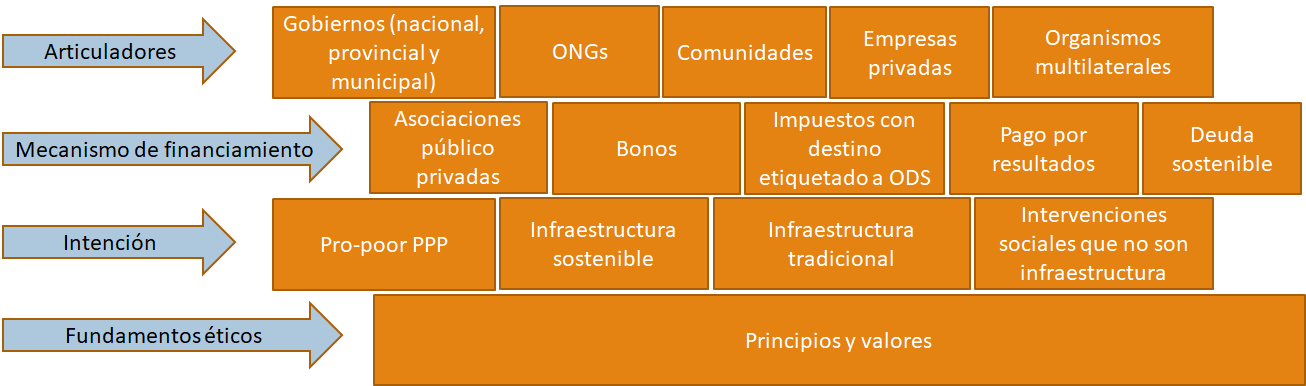

La Agenda 2030 no limita la creatividad de los actores para producir esquemas de financiamiento para alcanzar los 17 ODS. Por lo tanto, para ello pueden usarse desde esquemas tipo asociación público privada para el desarrollo de infraestructura sostenible, esquemas tipo Pro-Poor Public-Private Partnerships, bonos de impacto social y otros instrumentos de pago por resultados, deuda sostenible, impuestos o derechos especiales con destino etiquetado (por ejemplo para saneamiento de un río), entre otros. La siguiente imagen reproduce mi visión de cómo se construye el complejo entramado de actores, fuentes de financiamiento, tipos de proyectos y principios necesarios para implementar cualquier alianza público privada:

Cuadro 1. Bloques de construcción de las alianzas público privadas.

Fuente: elaboración propia

Como ha dicho la ONU, estas alianzas sirven para “movilizar, reorientar y aprovechar billones de dólares de recursos privados para generar transformaciones a fin de alcanzar los Objetivos de Desarrollo Sostenible.”[3] Por esta razón, la ONU incluyó a las alianzas como una de las metas del Objetivo 17 de la Agenda 2030: “17.17 Fomentar y promover la constitución de alianzas eficaces en las esferas pública, público-privada y de la sociedad civil, aprovechando la experiencia y las estrategias de obtención de recursos de las alianzas”.[4]

Uno de los puntos comentados durante mi presentación verso sobre los diferentes tipos de participación del sector privado en las alianzas. Además de inversionistas o empresas tradicionales, la participación privada en las alianzas también puede darse a través de empresas tipo B cuyo objetivo no es únicamente el generar utilidades a sus accionistas sino también generar beneficios sociales. Igualmente, la participación privada puede darse sin ánimo de lucro, a través de organizaciones de la sociedad civil, fundaciones, universidades, filantropías, por nombrar algunas.

Las alianzas público privadas pueden conformarse para el desarrollo de proyectos de infraestructura o bien para articular intervenciones sociales que no requieren de infraestructura. Sobre este último tipo de intervenciones tenemos como ejemplos esquemas de pago por resultados para aumentar la inserción laboral de grupos marginados; bonos de impacto social para aumentar la agricultura sustentable; intervenciones de bajo costo basadas en economía del comportamiento para motivar la reducción del consumo doméstico de agua (¡con tan solo cambiar la información de la factura de cobro del agua!).

Respecto a los proyectos para la construcción de infraestructura y provisión de servicios públicos, en los últimos años se han creado diferentes modelos que persiguen diferentes fines más allá del propio proyecto. Entre ellos encontramos las llamadas Asociaciones Público Privadas Pro Pobreza (en Inglés Pro-Poor Public-Private Partnerships o 5P), el modelo distributivo no lucrativo y la infraestructura sostenible.

Por ejemplo, las Asociaciones Público Privadas Pro Pobreza son una categoría creada para encuadrar modelos que buscan brindar acceso a servicios públicos básicos a las comunidades rurales o comunidades de bajos ingresos, generandoles ingresos propios y empoderandolas en el proceso. Entre estos servicios encontramos el acceso a electricidad (o a energía baja en emisiones de CO2), seguridad, agua potable, sanidad, educación, internet, por nombrar algunos de ellos. Como explica Sovacool este tipo de APP:

“involucra la participación de los gobiernos, compañías privadas, instituciones microfinancieras, bancos multilaterales de desarrollo, y organizaciones no lucrativas (incluyendo ONGs) [así como,] fabricantes de equipamiento técnico, compañías rurales de servicios energéticos, organizaciones filantrópicas, cooperativas, y los mismos hogares.”[6]

El autor revisó ocho estudios de casos en diferentes países de Asia y África, y concluyó que las APP del tipo 5P han permitido expandir el acceso a energía de comunidades en Bangladesh, China, India, Indonesia, Laos, Nepal, Sri Lanka y Zambia, y al mismo tiempo avanzar para alcanzar los Objetivos de Desarrollo Sostenible.

Un ejemplo inspirador es la puesta en marcha de la microhidroeléctrica de Cinta Mekar en Indonesia. Aquí, gran parte de su población con 640 hogares y más de 2 mil habitantes no contaba con acceso a electricidad, por lo que utilizaban keroseno y aceites para iluminación y cocinar sus alimentos. Para cambiar esta situación, se instaló una planta generadora de 120 kw de electricidad en el río adyacente cuyo costo rondó los $225 mil usd. ¿Cómo una pequeña comunidad rural puede financiar y participar en la gestión de un proyecto así?

En este caso, un inversionista privado financió parte del proyecto a cambio del 50% de las utilidades. Además, la ONU a través de UNESCAP (Comisión Económica y Social para Asia y el Pacífico) dió un crédito a la comunidad para pagarse solo después de que la planta estuviera en operación. La comunidad aportó tierras y trabajadores para la construcción de la obra. Además, la comunidad recibió capacitación de una ONG local, para poder supervisar algunos aspectos del mantenimiento de la obra. El gobierno de Indonesia, a través de su empresa estatal de electricidad, aportó un compromiso para compra de energía (excedentes) producidos por la planta de electricidad rural.

Los beneficios sociales de este proyecto han sido: 1) brindar acceso a electricidad a la población; 2) bajar las emisiones de CO2 al sustituir el uso de keroseno y quema de aceites por la producción limpia de la micro hidroeléctrica; 3) transformar a la comunidad en propietaria de una planta de electricidad; 4) generación de ingresos a la comunidad de 4 mil USD al mes (los cuales ya han utilizado para generar nuevos proyectos productivos de este tipo). Además de estar conectados con el Objetivo 1 y 7 de los ODS, estos beneficios tienen como resultado un activo intangible, pero muy valioso, que es el empoderamiento de una comunidad.

Proyectos como este demuestran que las alianzas público privadas son una herramienta importante para el desarrollo comunitario, pero como he mencionado también pueden ser usadas para proyectos con un impacto más grande, sea para el desarrollo municipal, estatal o federal. En este sentido, la reunión “Financiamiento para el Desarrollo Sostenible en el Ámbito Subnacional” fue un espacio que promovió el intercambio de experiencias, retos y modelos de financiamiento para la implementación de la Agenda 2030 a nivel estatal y municipal en México.

Mis agradecimientos más sinceros para los organizadores ONU (PNUD), GIZ, Oficina de la Presidencia de la República, CONAGO y el anfitrión el Gobierno del Estado de Tabasco; así como a todos los funcionarios públicos asistentes al evento y sus talleres. Dejo abajo algunas fotos para ilustrar la reflexión generada por los talleres y el entusiasmo de los asistentes.

[1] “Asociaciones Público Privadas en México:

Teoría, Derecho y Práctica”, tesis que para optar por el grado de Doctor en

Derecho presenta Yahir Acosta Pérez, Universidad Nacional Autónoma de México,

febrero 2019. Los 13 principios los deriva Krishnan Sharma de resoluciones de

la Asamblea General de la ONU y de la junta de expertos de la

Inter-agency Task Force on Financing for Development.

[2] Yahir Acosta y Ana Laura Barrón,

Transparencia y rendición de cuentas de las APP: recomendaciones de política

pública (Ciudad de México: Ethos, 2019), https://ethos.org.mx/es/transparencia-y-rendicion-de-cuentas-de-las-app-recomendaciones-de-politica-publica/

[3] Organización de las Naciones Unidas,

“Objetivo 17: Revitalizar la Alianza Mundial para el Desarrollo Sostenible”,

Objetivos de Desarrollo Sostenible. 17 Objetivos para Transformar nuestro

Mundo, http://www.un.org/sustainabledevelopment/es/globalpartnerships/

[4] Organización de las Naciones Unidas, Asamblea

General, RES/70/1 “Transformar nuestro mundo: la Agenda 2030 para el Desarrollo

Sostenible”, 21 de octubre de 2015, p. 31.

[5] Marrelli, Padovano & Rizzo, Servizi

pubblici: Nuove tendenze nella regolamentazione, nella produzione e nel

finanziamento, Milán, Italia; F. Angeli, 2017.

[6] Benjamin K. Sovacool, “Expanding renewable

energy access with pro-poor public private partnerships in the developing

world”, Energy Strategy Reviews 1, núm. 3: 181–92.